FSRA #

M22000227

BROKERAGE

Yournesta Financial

POWERED BY

Dominion Lending Centres

SERVING

Ontario-wide

Ontario Mortgage Tools & Services

Everything You Need to Plan, Compare & Get Approved

Instead of guessing your mortgage, use real Ontario calculations, compare lender options, and get expert guidance — all in one place. Whether you’re buying in Toronto, Vaughan, or anywhere in the GTA, this is your complete mortgage toolkit.

Mortgage Calculators (Ontario-Accurate)

Run the numbers using Ontario-specific rules — stress test, CMHC insurance, and Toronto land transfer tax included.

- Used by Ontario home buyers daily

- Built for Toronto & GTA market

- Works with real lender rules

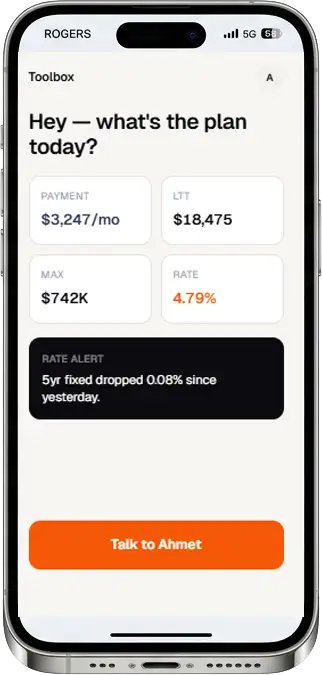

Download The My Mortgage Toolbox App

Download the Mortgage Toolbox App — access all nine Ontario mortgage calculators, real-time rate alerts, and direct one-tap contact with your mortgage advisor.

Take all Ontario mortgage calculators with you. Compare scenarios, track rates, and share results instantly — anytime, anywhere.

Ontario Mortgage Calculators

Free Ontario Mortgage Calculators Accurate for Toronto & GTA Buyers

Use our advanced Ontario mortgage calculators to plan your home purchase with real numbers — not estimates. Each calculator is built specifically for Canadian mortgage rules, including the stress test, CMHC insurance, and Ontario land transfer tax.

Ontario Mortgage Calculator Hub — All Tools in One Place

Access all nine Ontario mortgage calculators in one place — built to reflect real Canadian lending rules. Each tool includes stress test qualification, CMHC insurance, and Ontario-specific costs like Toronto land transfer tax.

What You Can Calculate

Run the numbers using Ontario-specific rules — stress test, CMHC insurance, and Toronto land transfer tax included.

- Monthly mortgage payments (principal & interest)

- Maximum mortgage affordability based on income

- Total cash required including down payment and closing costs

- Ontario and Toronto land transfer taxes with rebates

- Required income to qualify under the stress test

- Mortgage renewal savings and rate comparisons

Start With Numbers. Finish With a Better Rate.

Run your calculations, then get a personalized mortgage rate based on your real financial profile.

Every mortgage decision starts with the right numbers. This toolbox brings together all nine Ontario-specific calculators — from payment estimates to full purchase costs — so you can plan, compare, and move forward with confidence.

Built for the Toronto and GTA market, each calculation reflects real lender requirements used across Canada

Monthly Payment Calculator

Ontario Mortgage Payment Calculator

Calculate your monthly mortgage payment using real Ontario rules, including interest, principal, property tax, and CMHC insurance. Built for buyers across Toronto and the GTA.

Closing Cost Essentials

Ontario & Toronto Land Transfer Tax Calculator

Estimate your Ontario land transfer tax and Toronto double LTT instantly, including first-time buyer rebates. A critical cost for GTA home buyers.

Total Cost Breakdown

Ontario Closing Cost Calculator

Calculate your full closing costs, including legal fees, title insurance, land transfer tax, and adjustments. Know your true cash required before buying in Ontario.

Affordability Calculator

Maximum Mortgage Calculator Ontario

Find out how much mortgage you can afford based on income, debts, and the B-20 stress test. See what lenders will actually approve in Ontario.

Qualification Tool

Required Income for Mortgage Ontario

Estimate the income needed to qualify for a home in Ontario. Includes stress test rules and standard lender qualification ratios.

Lender Qualification Metrics

Debt Service Ratio Calculator Canada

Calculate your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios — the key numbers lenders use to approve mortgages in Canada.

Compare Mortgage Rates

Mortgage Rate Comparison Calculator Ontario

Compare two mortgage rates side-by-side and see the real cost difference over time. Understand how even small rate changes impact your total payments.

Mortgage Renewal Strategy

Mortgage Renewal Savings Calculator Ontario

Compare staying with your lender versus switching at renewal. See how much you could save over your next term with better rates.

Mortgage Agent Level 2

FSRA #M22000227

Your Ontario Mortgage Expert

Work With a Mortgage Agent Who Gets Deals Approved

I’m Ahmet Dogan — a licensed Ontario mortgage agent based in Vaughan, helping clients across Toronto and the GTA secure financing that banks often decline. I specialize in real-world scenarios: self-employed income, complex files, and buyers who need a smarter strategy to get approved.

If you’re searching for a mortgage broker near you in Vaughan, Toronto, Mississauga, or anywhere across the GTA — you’ve found the right place. I’m based at 665 Millway Ave in Vaughan and serve clients across Ontario, fully digitally. Most clients never need to visit an office.

If the numbers work, I’ll find the right lender. If they don’t, I’ll tell you honestly — and show you how to fix it.

Proven Results in the Ontario Market

$175M+ in funded mortgages across 300+ families in Vaughan, Toronto, and the GTA.

2× Top Producer at Yournesta Financial, powered by Dominion Lending Centres.

Access to 30+ Canadian Lenders

One application, multiple options. I work with banks, monoline lenders, credit unions, and private lenders to match your profile with the highest chance of approval.

Direct, Honest, and Fast

English & Türkçe support. You’ll get a response within 2 business hours — with clear answers, real numbers, and no pressure.

Google Reviews • Ontario Clients

Trusted by Ontario Home Buyers & Investors

Hundreds of clients across Toronto, Vaughan, and the GTA have worked with Ahmet to secure mortgages their banks wouldn’t approve — at rates their banks couldn’t match.

I highly recommend him !

Ahmet Thank you for helping our deal happen in such a timely manner! You are amazing!

Real Mortgage Results in Ontario

Recent Mortgage Deals — Real Results, Real Savings

These are real mortgage scenarios from clients across Ontario — including Toronto, Mississauga, and the GTA. Each file is anonymized, but the numbers reflect actual strategies used to secure better rates, approvals, and cash flow. From first-time buyers to renewals, refinances, and investment properties, these examples show what’s possible when your mortgage is structured correctly.

Every deal is different — run your numbers, then I build a strategy for your situation.

First-time buyer

Mississauga

$720K detached, 10% down

Renewal

Mississauga

$540K balance, switched lenders

Investor

Mississauga

$480K duplex, 4th property

Refinance

North York

consolidated debt, freed cashflow

Talk to an Ontario Mortgage Expert

Ontario Mortgage Questions

Frequently Asked Questions — Ontario Mortgages

Eight questions I answer every week — from first-time buyers in Vaughan to renewers across the GTA.

No. The Toronto Municipal Land Transfer Tax (MLTT) only applies to properties within the City of Toronto’s geographic boundary. Buyers in Vaughan, Mississauga, Markham, Brampton, Oakville, Richmond Hill, and all 905 municipalities pay only the provincial Ontario LTT — roughly half the total tax bill of a Toronto purchase. The boundary is tighter than most people expect. Use our Ontario Land Transfer Tax Calculator to check any specific address.

5% on the first $500,000 of purchase price, 10% on the $500,001–$1,500,000 portion, and 20% minimum on anything above $1,500,000. Anything under 20% down triggers CMHC mortgage default insurance — a premium of 2.8%–4.0% added to your mortgage balance. Our mortgage calculator handles all three tiers and CMHC insurance automatically.

OSFI’s B-20 guideline requires all federally regulated lenders to qualify you at the higher of your contract rate + 2%, or 5.25%. At today’s broker rate of ~4.79%, you’re qualifying at 6.79%. That single rule can reduce your maximum mortgage by $80,000–$120,000 compared to qualifying at your actual rate. Provincial credit unions are exempt from B-20 — in some cases this opens up a significantly higher purchase price. I’ll model both scenarios for your file.

Three programs every Ontario first-time buyer should stack: (1) Ontario LTT rebate — up to $4,000 provincial, plus up to $4,475 Toronto MLTT rebate if buying in the City of Toronto (combined max $8,475); (2) Home Buyers’ Plan (HBP) — withdraw up to $60,000 from your RRSP tax-free, repayable over 15 years; (3) First Home Savings Account (FHSA) — contribute $8,000/year up to $40,000 lifetime, tax-deductible going in and tax-free coming out for a home purchase. Used together, these programs can put $100,000+ of tax-advantaged down payment in reach for a two-person household.

Honest answer: it depends on your income stability, how long you’ll hold the property, and whether a $300–$400/month payment swing would create stress. Fixed locks in certainty for 5 years at ~4.79%. Variable is currently 120–160 bps lower (effective ~3.10%–3.55%) and benefits further if the Bank of Canada continues cutting. Historically, variable has outperformed fixed in approximately 70% of 5-year periods over the last 30 years — but fixed is the right call if rate uncertainty would affect your sleep or your budget. I’ll run both scenarios against your actual numbers, not ideology.

Almost never without shopping first. Banks send renewal offers at posted rates because 70% of Ontario homeowners sign without comparing. The gap between a bank’s posted renewal rate and what a broker can negotiate — at the same lender or a competing lender — is typically 40–80 basis points. On a $600,000 renewal balance, that’s $12,000–$19,000 in unnecessary interest over 5 years. Run your numbers in our Ontario Mortgage Renewal Calculator, then send me the offer. I’ll tell you within 24 hours whether it’s competitive or how much better you can do.

For a standard A-lender residential mortgage — purchase, renewal, or refinance — there is no cost to you. The lender pays a finder’s fee directly to the brokerage when your mortgage funds. You receive the same rate (or better) than going directly to the bank, at zero cost. A fee only applies on B-lender or private mortgage transactions, and I’ll disclose that amount in writing before any work begins — as required by FSRA.

For a straightforward purchase with clean T4 income documentation: pre-approval with a rate hold in 24 hours, commitment letter from the lender within 3–5 business days after an accepted offer, and closing on any date your real estate lawyer selects. Self-employed, investor, new-to-Canada, and complex income files typically take 7–14 business days. I set clear expectations on day one based on your actual file — no vague timelines.

Still Have Questions?

Not seeing your exact situation here? Let’s take a look at your numbers and walk through your options step by step.

Ontario Mortgage Blog

Ontario Mortgage Insights — Written by a Broker, Not a Copywriter

Plain-language analysis on rates, renewals, first-time buying, and GTA market conditions. Published when something worth saying happens — not on a content calendar.

-

How Much Home Can You Actually Afford in the GTA in 2026? (After the Stress Test)

The number your bank pre-approval shows you and the number the stress test actually lets you borrow can differ by $100,000 or more. Here’s what the B-20 qualifying rate means for real GTA households — with actual income-to-price examples across Toronto, Vaughan, and Mississauga. -

FHSA, HBP, and the LTT Rebate: How Ontario First-Time Buyers Stack All Three in 2026

Most first-time buyers in Ontario know about one of these programs. Very few know how to combine all three — or in what order. Done right, you can put $100,000+ of tax-advantaged money toward your first home and save up to $8,475 at closing. -

Self-Employed in Ontario? Here’s How Lenders Actually Read Your Income in 2026.

Banks see write-offs. The right lender sees income. If you’ve been running a business for 2+ years and a bank just said no — or you’ve been afraid to apply — there are three documentation pathways available to you in Ontario right now. Most brokers only know one of them.